Ask the Expert: What to do after losing all savings in a scam?

Question 1

- We are receiving a half pension but recently lost all our savings through an investment scam. Our house is worth $1.5 million. Is a reverse mortgage a good option? How exactly does it work?

Sorry to hear about that. ASIC’s Moneysmart website has information on scams and how to protect yourself.

With investment scams and failed investments, it might be worth contacting Centrelink’s Financial Information Service who may be able to assist, as I note you are still only receiving half of the age pension.

A reverse mortgage is an option at least worth considering. This means taking out a loan to provide you with a lump sum and/or ongoing income payments. The lender would take security over your home and the debt would need to be repaid when the home is sold or upon death.

These types of arrangements are becoming more popular. And providers should be offering a no-negative equity guarantee (so the loan can never be more than what the home is worth).

The downside is you will have less equity in your home. This may or may not bother you. If you plan to leave funds or assets to your children or other beneficiaries, this will affect them.

You might like

Depending on how much you need, you could just obtain a small loan.

The government’s Home Equity Access Scheme is a good place to start. It’s a fairly conservative scheme that only allows minimal lump sums and ongoing fortnightly payments of up to 150 per cent of the age pension. In this way the loan only increases slowly.

If you were looking for larger payments you would need to use the services of a retail reverse mortgage provider, such as Household Capital.

Reverse mortgages certainly have their place, but it’s a big decision so you should seek advice first.

An alternative option to consider is to downsize and free up some of the money currently tied up in your $1.5M home.

Question 2

- I am in the fortunate position of having a large superannuation balance of $1.9M with my construction industry super fund. I am 67, turning 68 in December. My account is still in accumulation phase. The components are $734,000 tax free and $1,168,000 taxable. I have no dependents and would like to take advantage of the ‘cash out and re-contribution strategy’ starting with what remains of this financial year.

My closing account balance at the end of last financial year was $1,784,000. Because of the size of my balance I am running into difficulty with the non-concessional contribution caps, if I want to use the bring forward rule a couple of times before I’m 74. A nice problem to have I know, but I haven’t had much joy when I’ve spoken to the Cbus advice team, who seem to default to trying to persuade me to begin an income stream before I’ve dealt with this estate planning issue of the ‘death tax’.

I have two questions. Can the ‘cash out and re-contribution strategy’ also be applied during the pension phase, or only while still in accumulation phase? Is my only solution to my problem with the non-concessional contribution caps and the bring forward rule, to withdraw a large lump sum, for example $400,000 before the end of this financial year? Thanks for any information you can provide.

Cash out and recontribution strategies are a fairly popular strategy for those who don’t want their future beneficiaries paying tax on the proceeds of your super. I covered this in a previous article.

Stay informed, daily

To come directly to your questions:

- Yes, you can perform a cash out and recontribution strategy while in pension phase. You just need to have an open accumulation account to put the money back into. The other requirement is that you must be under the age of 75 when you contribute.

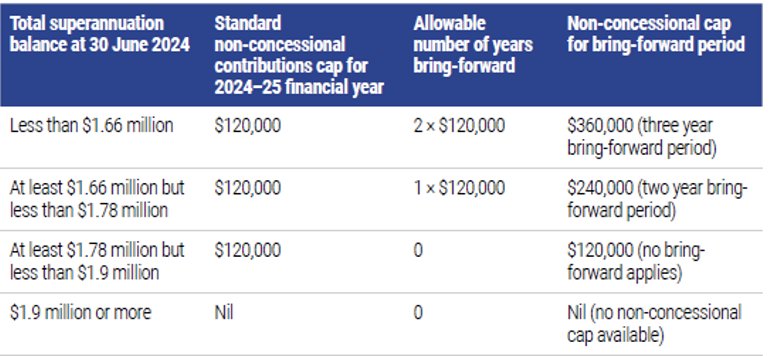

- Yes, you could withdraw some funds from super or pension just before the end of a financial year. This may allow you to end up contributing the funds back in once the new financial year commences. That is because the ‘Total Super balance’ is only measured once a year, on June 30. The below table provides a guide on how much you can contribute based on the June 30 balances.

Question 3

- My wife and I are receiving the age pension from Poland. It’s about $1400 all together per month. How will this affect our age pension when we apply for the Australian age pension?

Australia has social security agreements with 32 countries, including Poland, these can be found here.

The agreements can be complex so you will need to speak with Centrelink about your personal circumstances. However, broadly speaking, the following would apply:

People who live in Australia but do not have 10 years’ residence in Australia can count their Polish periods of insurance to qualify for an Australian pension, subject to the means-test.

During this time (until they have 10 years’ residence in Australia) they are paid the normal means-tested pension rate less the amount of any Polish pension – that is, the Polish pension is ‘topped-up’ to the rate of the Australian pension they would receive if they had no Polish pension.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.