Ask the Expert: When playing ‘catch up’ with super can pay off for retirement

Question 1

I have been on leave without paying super from July 1. I want to put $30,000 concessional super and $23,000 catch up super into my fund this financial year. Is this possible if I don’t return to work? I have capital gains on an investment property I sold in July, which gets added to income. Am I allowed to do this to offset the tax?

Hi there,

Concessional super contributions are made up from the following types of contributions:

1. Employer Super Guarantee

2. Salary sacrifice

3. Personal contributions where you claim a tax deduction.

The normal annual concessional cap is $30,000 but as you have indicated you may be able to use ‘catch-up’ contributions where you didn’t fully use the concessional cap in previous years and your total super balance is below $500,000.

You might like

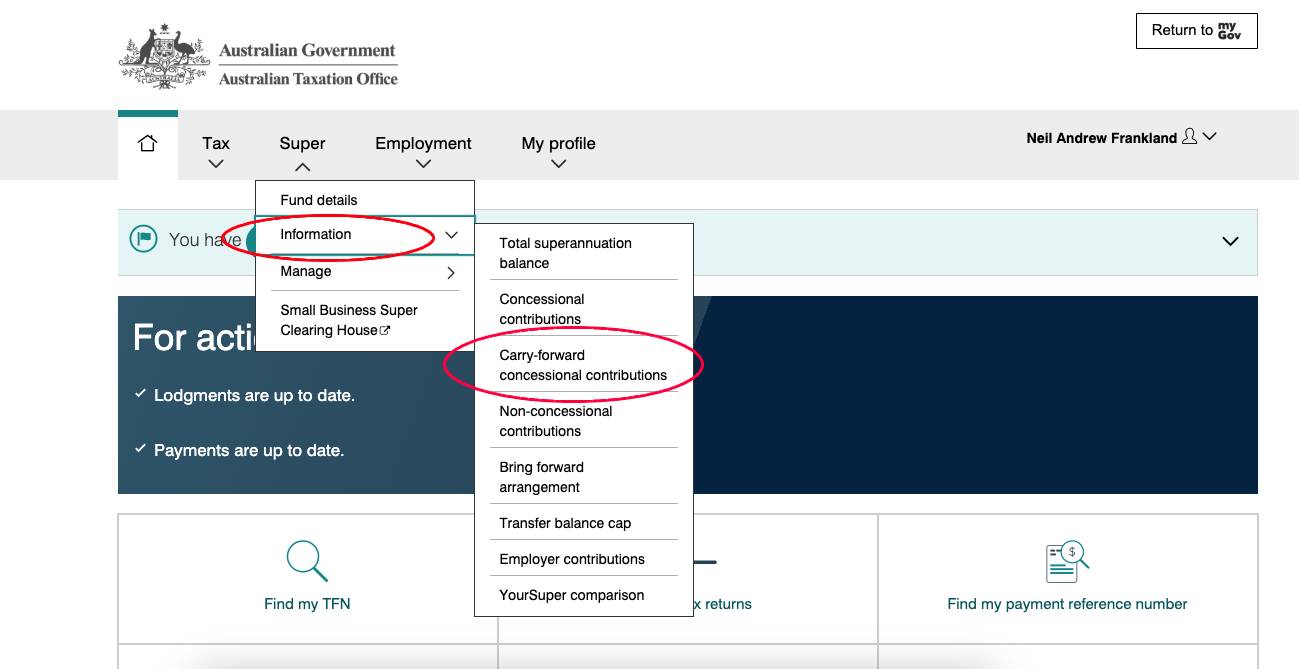

The best way to check is to login to MyGov, visit the Australian Taxation Office site and view your available amount, as per the screenshot below.

If you are not working, then you can claim personal tax deductible contributions only up until age 67. Otherwise, you would need to meet a work test.

Selling an asset that will provide large capital gains and then using the carry forward concessional contributions is a popular and effective strategy.

Capital gains are added to your taxable income and tax paid via income tax (some people mistakenly believe capital gains tax is a separate tax).

Therefore, making concessional super contributions both reduces your income tax and builds up your retirement savings.

You can only claim a tax deduction up to an amount that equals your assessable income. For any surplus funds you could look to contribute those funds to super as a non-concessional contribution.

Question 2

I am 59 soon and am going to transfer my super into an account-based pension when I turn 60. My super account is split into three investments – balanced, international shares and index diversified. When I switch, how are the investments handled? Do they stay the same or is the pension fund at a variable percentage blanket rate?

When you start a pension, you will be asked how you want to invest the funds.

Stay informed, daily

It’s an opportune time to review your risk profile to ensure your investment mix is something you are comfortable with. Your funds could still be invested for another 25-30 years, so it’s an important decision.

Depending on your super fund, there will also be different tax consequences to consider.

Most industry funds have already factored in any tax within their unit prices, so you wont explicitly have to pay tax when you rollover from super to pension.

Many of them have something called a retirement bonus or income booster (or something similar). This is when you rollover your super to a pension with the same fund and the same investment options, you receive a one-off payment.

The payment represents a refund of accrued capital gains tax liability that the fund would no longer have to pay. If you are with an industry fund, you should check if it offers this.

If you are with a wrap or master trust-style super fund, capital gains tax is applied at an individual level. This means it is not reflected in the funds unit price (so price would be higher).

However, the tax would have to be paid upon exit. Unless you again rollover the existing investments into the same provider.

Going into pension you should look at obtaining some personal advice or at a minimum speak with your super fund to see what they offer.

Question 3

I have an allocated pension with a balance of $1.5 million. I have savings of $200,000 earning 5 per cent (I will have to pay tax on the interest). Can I put the savings into my allocated pension? I am 68.

Any drawdowns and interest earned from your account-based pension are tax free.

I assume you must have other taxable income if you are saying you are paying tax on your interest. The effective tax-free rate – the rate before having to pay income tax (taking into accounts various offsets) is $22,575, but for a single senior or pensioner its approximately $35,813.

While you can’t directly add to your existing pension, you can add the funds to super via an after tax non-concessional contribution.

You can then start a separate pension with these funds, or roll your existing pension back to super, add the funds together and start a new combined pension, ensuring you remain under your Personal Transfer Balance Cap.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.